Buffalo Potash ($BUFF.V)

Lessons on Fertilizer Beneath the Prairie

TL;DR: Buffalo Potash is a junior miner trying to extract potash in Saskatchewan using horizontal drilling methods borrowed from oil & gas - cheaper than conventional methods, but unproven at commercial scale in potash.

The team is credible (they helped discover, build and operate adjacent mines), the geology is de-risked by major producers, and the modular approach is designed to avoid the financing death trap that killed the last company to try this. The path from here: assay results late March (in progress), PEA (also in progress), ~C$30M raise, then first production 12-18 months later.

Key risks are technology execution and financing. Key upside: if it works, the numbers suggest a 4-8x return from current levels.

What Exactly is Potash? A Light Primer

Potash is a water-soluble, potassium-based fertilizing mineral. Along with nitrogen and phosphorus, it’s one of the three essential nutrients that virtually all commercial agriculture depends on. Supply was historically stable, but creeping de facto autarky has shifted the priority from price to security-of-supply. The well-documented April 2022 spike above $1,200/t demonstrates how quickly this market can reprice when guaranteed food supply flows are disrupted. While prices have retraced, the backdrop has changed; resource nationalism, sanctions and fragmented trade blocs have catalyzed a tight supply-demand dynamic.

So we now have a credible case for a durable move higher if marginal supply requires materially higher incentive pricing. Where will this supply come from? New projects are capital intensive, long-dated and execution-sensitive. Consider BHP’s behemoth Jansen Project, which in recent memory has seen production delays and upward capex revisions. As for poor execution, look at Western Resources’ perpetually underfunded attempt resulting in insolvency (discussed later). With that context, higher long-term prices may be necessary to justify development and to ensure reliable supply in an increasingly fractured market.

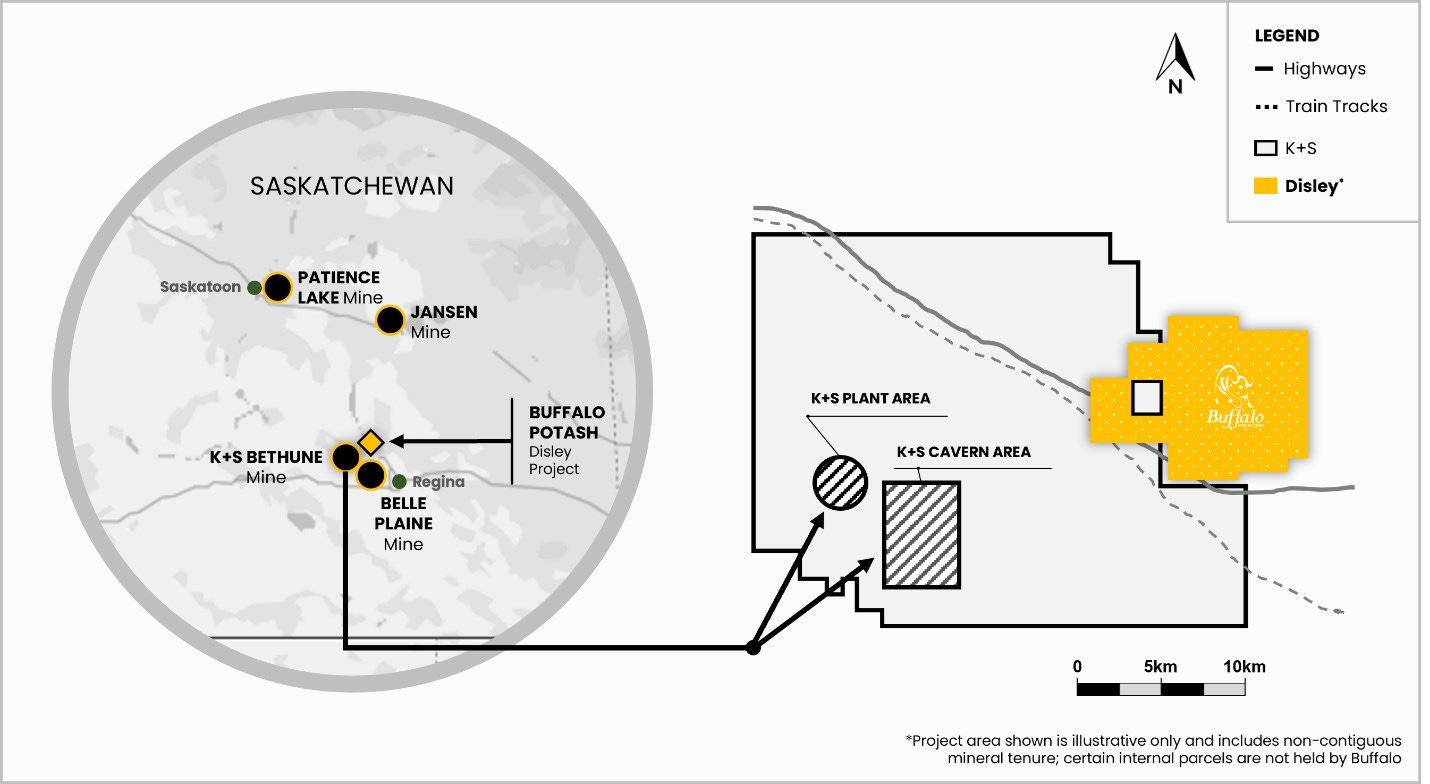

Saskatchewan is the “Saudi Arabia of potash”, and produces about 32% of the world’s supply. The province sits on vast and shallow uniform beds of the stuff, deposited 440 million years ago when a seabed evaporated and left behind its mineral salts in flat layers stretching hundreds of kilometers in every direction. This matters for what Buffalo is trying to do.

How Potash Is Usually Mined

There are two conventional approaches.

Traditional underground mining: sink an expensive shaft 1,000 meters into the earth, mechanically extract potash and haul it to surface (capital-intensive and slow to build).

Solution mining: drill vertical wells down to the potash beds, pump water in, dissolve the mineral into a brine, pump the brine back up, then crystallize out the potassium chloride on surface. Several large mines in Saskatchewan already use this method - including K+S Bethune and Mosaic Belle Plaine, both of which happen to sit immediately adjacent to Buffalo’s Disley Project property.

Solution mining is cheaper than shaft mining, but it still typically requires many vertical wells to cover sufficient area.

Buffalo’s Proposal: Horizontal Wells

Buffalo’s core technology borrows what the O&G bros figured out twenty years ago: horizontal drilling. Their team have genuine experience here as they previously worked on a steam-assisted gravity drainage heavy oil project that sold to Husky. So, if the equipment, contractors, and operational knowledge already exist in the province, then the conceptual leap to potash solution mining is smaller than it sounds, in theory.

Instead of drilling dozens of vertical wells down into a potash bed, one drills three horizontal wells that run laterally through the potash bed itself. The economics are meaningfully better: lower capex, lower opex, and a modular structure that lets you scale up incrementally rather than committing hundreds of millions upfront. Once a horizontal plane is exhausted, the operation expands vertically into adjacent beds - the geology should permit this through the consistent potash beds.

However, they are not the first to try this; Western Resources attempted horizontal drilling too, and their execution of this idea sent them into effective bankruptcy. So if the technology is not the differentiator, then the approach must be.

What’s changed vs. Western Resources

The lesson from Western Resources that Buffalo seems to have internalized is modularity. The pitch is don’t build the whole thing at once with borrowed money, build small, prove it works, generate cash flow, expand incrementally. This should avoid the death trap Western fell into - a project that was near completion, yet ran out of money and was unable to cross the finish line. Buffalo’s team is also more operationally credible. Their advisory bench includes the likes of Peter Jackson who clocked 35 years at Mosaic (VP of North American Potash Operations). There is a material difference between “I raise money for projects” and “I ran Belle Plaine.”

Nevertheless, some similarities remain. They are at confirmation drilling stage with no potash production and a long path ahead: feasibility study, permitting, construction financing, construction, commissioning. Every one of those is a hurdle. The question is simple: Can they reach cash flow positive on Phase 1 before needing to raise money for Phase 2? If yes, the flywheel starts. If Phase 1 runs overtime or overbudget (and construction projects almost always do), they risk ending up exactly where Western did.

The Property

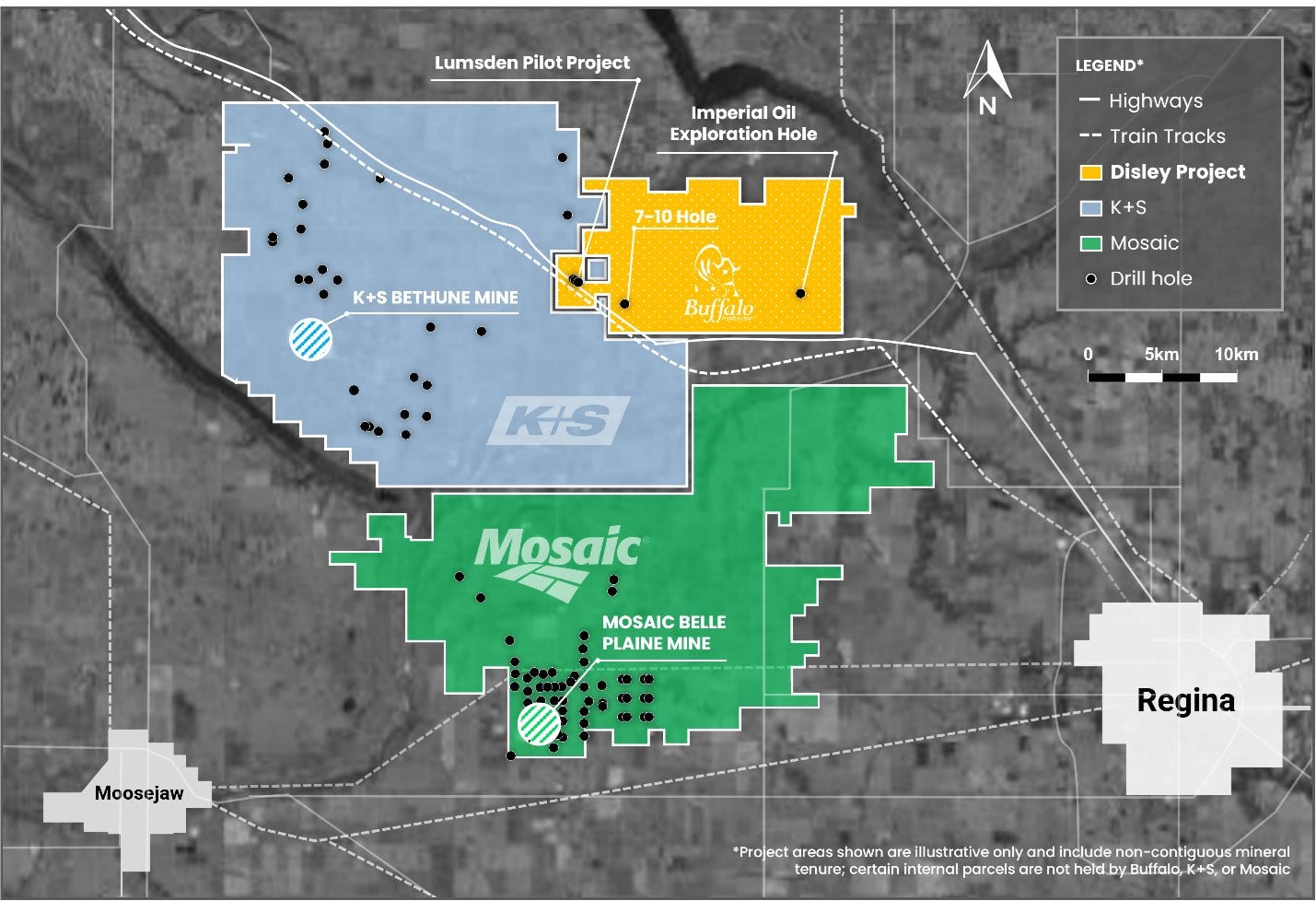

The Disley Project covers 9,413 hectares about 50km northwest of Regina, with K+S Bethune to the east and Mosaic Belle Plaine to the south. That adjacency soothes my concerns re: geology. The potash is evidently there, the question is whether Buffalo’s technology can extract it economically.

Saskatchewan potash is predominantly sylvite, which dissolves readily in solution mining. The chemistry is standard: brine dissolves potassium chloride preferentially depending on temperature and salinity, and the solution is processed at surface into dry crystals. Buffalo have a patented mechanical crystallizer that reduces the cost of this separation step, and crucially, their process proposes recycling water - relevant for the prairies. They will likely be drawing on the Mannville Formation brine at 550m depth rather than fresh water, which matters both for operating costs and for not competing with agricultural water users. The property also has road and rail infrastructure in place (white lines in graph).

Two 1960s drilling programs - the Lumsden Pilot Project on the western side and an Imperial Oil exploration hole on the east - left behind core samples now being re-assayed by the Saskatchewan Research Council.

The first modern confirmation hole, completed February 2026 to 1,563 meters, intersected all targeted potash-bearing members of the Prairie Evaporite Formation with 98%+ core recovery. Assay results are expected mid-to-late March. A 45km² 3D seismic program will connect existing 2022 coverage across the full property. Together, the legacy cores, the new drill hole, and the seismic data feed into an integrated geological model that underpins the forthcoming NI 43-101 report.

The Team and Track Record

The CEO and technical lead is Steve Halabura; he’s the person who originally “put the X on the ground” on what became the K+S Bethune mine (Radius Research: watch this video). They describe themselves as Saskatchewan potash specialists, not generalists.

Jansen Mine: CEO Halabura was part of the Anglo Potash Ltd. team that sold the Jansen potash project to BHP.

K+S Bethune Mine: CEO Halabura co-founded foundational assets; COO Hardage led exploration & drilling design

Patience Lake: CEO Halabura contributed to early-stage studies exploring solution mining optimization.

Director Peter Jackson has worked at all of Mosaic’s potash business unit sites.

Capital Structure and the Development Plan

Buffalo went public via RTO in January 2026 at $0.25/share, and has 109.5 million shares outstanding fully diluted with 45.7 million subject to voluntary lockup. The C$7.8M in the bank funds the first milestone: confirmation drilling, 3D seismic, and the technical work to produce a PEA.

Q1 2026: Assay results from the legacy cores and the first confirmation drill hole. 3D seismic program underway to map the potash beds precisely and identify sweet spots for horizontal well placement.

End-April / Early-May 2026: PEA and NI 43-101 mineral resource estimate. De-risk and re-rate.

Mid-2026: Second capital raise, targeting an additional C$20-30M to fund the first commercial demonstration: a triplet of horizontal wells targeting 125,000 t/year production. Project debt financing is part of the structure here - not pure equity dilution.

12-18 months post-raise: First production.

The capex on that first module is estimated at C$30M for 125kt. Buffalo has already been approached by buyers wanting a dedicated supply of 200-300kt per year. In fact, this scenario goes further than a standard offtake: CEO Halabura has spoken to these parties to potentially fund the expansion from 125kt to 250kt or beyond in exchange for dedicated supply (per interview). If that materializes, it largely solves the financing risk that has killed junior potash developers before.

Risks Recap

The Honest Risks of HLD. Horizontal drilling in potash has not been commercially demonstrated at scale. CEO Halabura acknowledges that there will be unknowns when the first wells go in. What reduces the geological uncertainty is that the Disley property has legacy 1960s solution mining test data, and the 3D seismic program will be critical for identifying sweet spots and avoiding problem zones before committing drill pipe. While vertical wells remain a fallback, that would materially weaken the economics that make this interesting in the first place, and would make this investment a non-starter (for me).

Financing risk. Buffalo has enough cash to reach the PEA and resource estimate milestone. Getting from there to production requires a $20-30M raise in a market that has been fickle toward junior miners. If the raise is difficult or dilutive, the economics change.

Execution risk. The 3D seismic is partly about confirming the beds are where they expect them to be. There’s some chance the horizontal wells encounter structural surprises - faults, bed discontinuities - that complicate things. This is mitigated by working in the most geologically consistent potash jurisdiction on earth, but it can’t be ruled out entirely.

The Valuation Setup - Quick Maffs Scenario

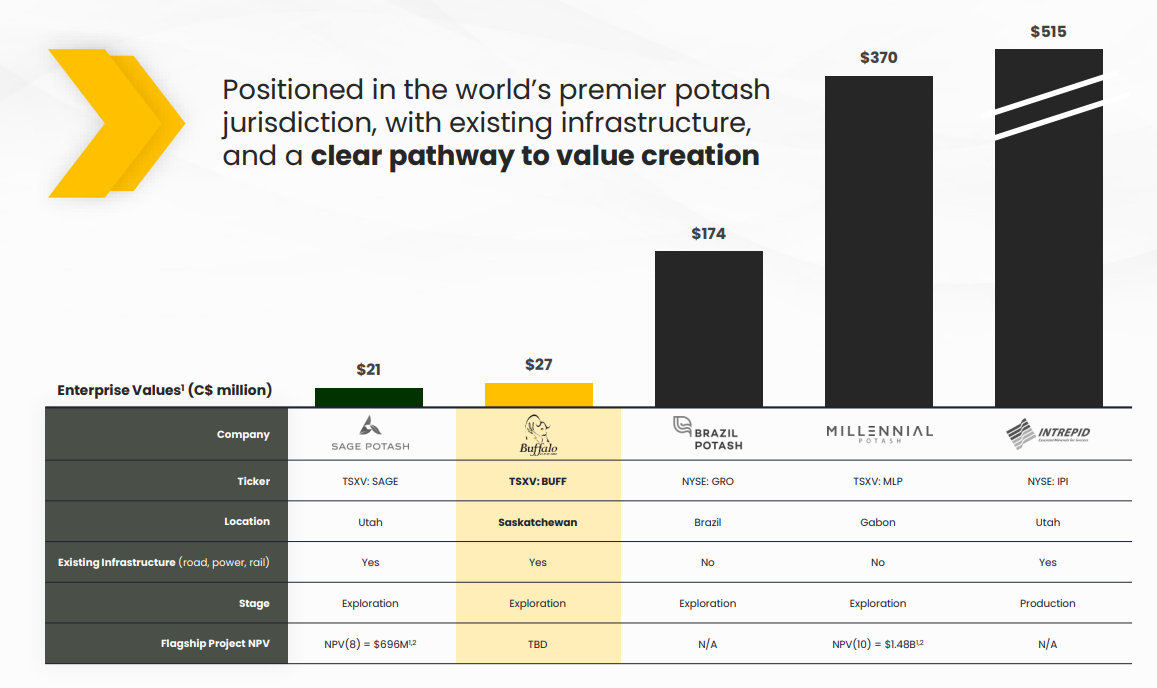

On a fully diluted basis, 109.5M shares at C$0.32 implies a market cap of ~C$35M and an enterprise value of ~C$27M (net of C$7.8M cash). Post-PEA, assume a C$30M raise split evenly between project debt and equity at C$0.50/share, issuing 30M new shares for ~140M fully diluted.

At 125kt/year and a C$200/t netback, gross operating cash flow is C$25M. After sustaining capex, provincial taxes and royalties (~C$6M), free cash flow could be approx. C$19M. At a 6x multiple - a discount to established producers reflecting single-asset and technology risk - that implies C$114M enterprise value, or ~C$0.71/share after netting debt: a 2.2x return from current levels.

Scale to 250kt/year (funded by offtake partner, no incremental dilution) and FCF roughly doubles to ~C$42M. At the same multiple, equity value reaches ~C$237M, or C$1.69/share - a 5.3x return with no change in potash prices.

The table below stress-tests across three scenarios varying netback (C$150–250/t), FCF conversion, and valuation multiple (5–7x):

Layer in the macro backdrop where new supply requires materially higher prices to justify greenfield development, and the upside extends further still.

*The C$200/t netback remains the key variable. If HLD delivers the cost structure management projects, the base and bull cases hold. If opex disappoints, the bear case still returns capital at Phase 1 and offers some upside at Phase 2.

Why I’m Watching This

The setup is straightforward: a credible team working proven ground with a proposed differentiated cost structure. The stock has been weak since its IPO as early stage investors dumped their cheap stock in the first few weeks (to ride the warrants), which has left the price quite depressed still.

Today (23rd Feb 2026), Buffalo engaged Micon International to prepare the NI 43-101 resource estimate and PEA, with release expected end of April. Assay results from the first confirmation hole are also due mid-to-late March, running in parallel with re-assay of the 1960s legacy cores. While these releases won’t guarantee the project’s execution, they will likely lead to a re-rate. With that in mind I’ll likely be adding on any price weakness until then.

Not financial advice, just talking about what I’m up to.

This is really good work mate. I'm a buyer based on this...